Abstract

In response to growing scrutiny surrounding commodity-driven deforestation, companies have introduced zero-deforestation commitments (ZDCs) with ambitious environmental and social targets. However, such initiatives may not effectively reduce deforestation if they are not aligned with the spatial extent of remaining forests at risk. They may also fail to avert socio-economic risks if ZDCs do not consider smallholder farmers' needs. We assess the spatial and functional fit of ZDCs by mapping commodity-driven deforestation and socio-economic risks, and comparing them to the spatial coverage and implementation of ZDCs in the Indonesian palm oil sector. Our study finds that companies' ZDCs often underperform in four areas: traceability, compliance support for high-risk palm oil mills, transparency, and smallholder inclusion. In 2020, only one-third of companies sourcing from their own mills, and just 6% of those sourcing from external suppliers, achieved full traceability to plantations. Comparing the reach of ZDCs adopted by downstream buyers with those adopted by mill owners located further upstream, we find that high-quality ZDCs from buyers covered 62% of forests at risk, while mill owners' ZDCs only covered 23% of forests at risk within the mill supply base. In Kalimantan and Papua, the current and future deforestation frontiers, the forests most at risk of conversion were predominantly covered by weak ZDCs lacking in policy comprehensiveness and implementation. Additionally, we find that only 46% of independent smallholder oil palm plots are in mill supply sheds whose owners offer programs and support for independent smallholders, indicating that smallholder inclusion is a significant challenge for ZDC companies. These results highlight the lack of spatial and functional alignment between supply chain policies and their local context as a significant gap in ZDC implementation and a challenge that the EU Deforestation Regulation will face.

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. Introduction

The expansion of oil palm plantations has been a key driver of deforestation in Indonesia in the past two decades [1, 2]. Due to increasing global demand, palm oil production is expected to lead to the loss of 13% of Indonesia's remaining natural forests by 2050 if historical trends persist [3]. At the same time, the oil palm sector has reduced rural poverty, contributed to Indonesia's economic growth [4–6], and has historically been supported by Indonesian public policies [7]. While forest-focused public policies such as moratoria on land permitting and forest conversion have contributed to forest governance improvements, they historically had a small impact in halting deforestation [8, 9] due to limited coverage, compliance, and enforcement [8, 10].

In response to this perceived public governance gap and increasing transparency about the role of specific multinational companies in sourcing deforestation-linked products, pressure on companies from civil society organizations to take action to help halt deforestation has grown. NGO campaigning, naming and shaming campaigns, and increased sectoral commitments to help address deforestation have stimulated companies in the palm oil sector to adopt zero-deforestation commitments (ZDCs) [11]. ZDCs are corporate pledges made by companies to not purchase products grown on land cleared after a certain cutoff date [11–14]. To assess the likely effects of such private policies, it is crucial to understand both their policy design and spatial patterns of implementation.

Companies typically put their individual or collective ZDC pledges into action by changing internal company policies and implementing stricter sourcing criteria and codes of conduct for their suppliers [11]. Third-party or roundtable certification standards are often used as a way to verify a product met these criteria [12]. ZDC policies differ in policy characteristics, scope, stringency, implementation, transparency, and effectiveness [11, 12, 15, 16]. While ZDC policies may include purchasing certified products (such as, in the case of palm oil, oil certified by the Roundtable on Sustainable Palm Oil [RSPO]), they also include efforts to improve supply chain traceability, supplier monitoring and engagement, and the implementation of grievance systems that allow aggrieved third parties to alert companies to policy non-compliance within the supply chain [16].

ZDCs tend to be adopted by large downstream companies (e.g. consumer goods manufacturers and refiners) who then have to disseminate their requirements to upstream actors such as oil palm mills—who process fresh fruit bunches (FFBs)—and the plantations on which oil palms are grown [15, 16] (see figure 1). In addition, many ZDC companies own oil palm mills and associated plantations themselves, directly implementing their commitments within their operations [17]. When pursuing best practices, ZDC companies observe their sourcing areas using satellite monitoring and use their purchasing power and engagement strategies to convince mills and plantations in their supply chains to avoid converting forests. They also stop purchasing FFB from producers who convert forests and require non-compliant producers to adopt their own ZDCs and in some cases to remediate damage caused before allowing them back into their supply chain [17]. While previous research has identified a number of challenges to implement ZDC policies in this ideal way, ranging from a lack of accurate mapping and traceability data to conflicts with buyers' conventional procurement practices, companies have increasingly gained experience and experimented in overcoming such limitations [11, 15, 18]. Still, the range of quality of ZDC policy design and implementation across companies has been underexplored to date.

Figure 1. (a) Simplified palm oil supply chain, (b) the policy stages of ZDC implementation across the supply chain [16]. In figure (a), plantations, mills, and refineries with red icons are owned by the same corporate group; when connected by red arrows, it represents an integrated supply chain (middle); in many cases, an independent mill company may source from its own plantations and farmers (right). The supply chain icons in figure (a) are highlighted in a lighter color to correspond to their respective policy stages in figure (b).

Download figure:

Standard image High-resolution imageFurthermore, even when a policy is comprehensively designed and implemented, it may still fail to reach its desired environmental outcomes if its reach does not match the biophysical conditions on the ground. To enhance the likelihood that ZDCs will reduce deforestation and prevent diversion of deforestation into other areas [19], ZDC implementation should be targeted toward forests at risk of conversion. Not all forests are equally vulnerable to conversion due to varying levels of anthropogenic pressure, such as topography, infrastructure, and proximity to established agricultural lands [20]. Yet, companies with strong ZDCs may selectively source from regions with little remaining forest at risk, which would undermine the conservation effects of their policy.

Additionally, policies that do not take into account local socio-economic contexts may create unintended consequences such as the exclusion of vulnerable producers. Introducing new sourcing policies without safeguards for marginalized communities, such as oil palm smallholders, may harm their livelihoods. Given that smallholder communities have a lower capacity to adapt rapidly to more stringent sourcing requirements, they are at risk of being excluded from international markets and experiencing worse prices, purchasing conditions, or a total lack of marketing options unless companies support them by strengthening their adaptive capacity or ensuring their market access [16–18, 21].

Previous research assessing the impacts of oil palm ZDCs is limited due to data gaps on company-specific oil palm supply chains, and ZDC characteristics and implementation. One recent ex-ante modeling study suggests a 25% reduction in deforestation would be possible if ZDCs were to successfully restrict future expansion in forest areas in Sumatra, Kalimantan and Papua [22]. Yet, to our knowledge, the distinct effects of ZDCs adopted by distant buyers versus local owners of plantations has not been explored. Although there are no ex-post assessments of the impact of oil palm ZDCs, a larger body of literature focuses only on assessing the impact of the RSPO certification [23–28] in lieu of data on ZDCs. Because these studies have not considered the diversity of ZDC policy designs beyond the RSPO, they provide only a partial view of the complex reality of private sector action. Understanding these gaps is particularly urgent considering the 2023 EU Deforestation Regulation (EUDR), which established mandatory due diligence requirements for forest-risk commodities [29]. Corporate compliance with this law will likely build on the extant private commitments, which makes a thorough understanding of their strengths and limitations crucial for meaningful regulatory implementation.

To address these concerns, here we examine the spatial and functional fit of ZDCs in the Indonesian oil palm sector via an ex-ante approach to policy evaluation [30, 31], which aims to provide plausible impact pathways [32] and is considered an effective way to analytically anticipate the potential outcomes and consequences of a policy [33]. We ask three questions: (1) How comprehensive are ZDC policies in supply chains handling Indonesian palm oil? (2) What is the spatial fit of ZDCs, i.e. the alignment between the geographical scope of ZDCs and forests at risk? (3) What is the functional fit of ZDCs, i.e. the degree to which companies incorporate local socio-economic contexts in their policies? Following Moss [34], we define spatial fit as the alignment between the geographical scope of a governance arrangement and the ecological system it addresses. Previous research has explored the relevance of the spatial fit concept in the context of global commodity flows [33–36]. We present the first attempt to apply this concept to data-intensive analysis and additionally examine the functional fit of ZDCs, which we define as the alignment between a governance arrangement's policy design and the local socio-ecological contexts it addresses (see also [37]). We examine functional fit by assessing the extent to which smallholder oil palm producers are located in supply sheds covered by ZDCs that include equity-related considerations for supporting smallholder farmers [12, 16].

2. Conceptual framework

2.1. Defining ZDC quality and evaluation criteria

Effective ZDCs require stringent commitments with clear targets about what is to be conserved and by when, implementation strategies, functional and transparent mapping and monitoring, and verification [12, 38]. The benefits are reinforced if companies that control a significant share of global commodity markets collectively target areas at risk of commodity-driven deforestation [12]. The effectiveness of ZDCs also relies on supportive regulatory, political, and financing conditions [12] and synergistic public-private interactions [39]. For example, the capacities of companies to monitor individual suppliers are influenced by whether the regions in question have clear tenure arrangements and public land registries that can be accessed. Ultimately, to ensure equity in access, ZDCs should include producers with different adaptive capacities (i.e. the capacity to adapt to changing market conditions and expectations) [16], which may contribute to enhancing rural livelihoods [21].

We focus on assessing the quality of ZDCs based on both policy design and implementation. We identify six components of a comprehensive ZDC policy: (1) commitment to zero deforestation and no planting on peatland covering all suppliers; (2) commitment to 100% traceability to mills and plantations; (3) support for smallholders; (4) support for mills at high risk of contributing to deforestation; (5) functional grievance system; and (6) transparency. For each of these components, we identified minimum cut-off points in performance that determined whether companies were assessed to have a high-quality ZDC. Table 1 illustrates our six principles that were adapted from past work on ZDC effectiveness and equity [12, 16], as well as the corresponding included evaluation criteria.

Table 1. Evaluation criteria for comprehensive ZDC policy in the palm oil sector. The principle categories were adapted from [12, 16], the evaluation criteria adapted from SPOTT (Sustainable Palm Oil Transparency Toolkit), a non-profit platform that monitors company pledges and implementation [40]. Detailed explanation of the principle categories and criteria can be found in supplementary table 1S. SPOTT also differentiates the score based on, for example, the level of transparency, disclosure, verification, etc.

| Principle categories | Evaluation criteria |

|---|---|

| Conservation commitment | 1. Conservation commitment includes pledge on deforestation- and forest conversion-free supply chain |

| ZDCs should be stringent with clear targets, geographical scope, and commitment to no deforestation and no planting on peatland. | |

| 2. Commitment to not planting on peatland | |

| Traceability | 1. Timebound commitment to achieve full traceability to mill |

| ZDCs should have a time-bound commitment to achieve traceability to both mill and plantation levels for their own and suppliers' plantations as well as report their traceability progress. | 2. Timebound commitment to achieve full traceability to plantation |

|

3. Traceability implementation to mill

| |

| 4. Traceability implementation, from own mills to plantation | |

| Smallholder inclusion | 1. Design program to support independent or scheme smallholders |

| ZDC should provide programs to support smallholders, for example via capacity building, that are differentiated for different types of smallholders with a clear informed target. | |

| 2. Participation of independent or scheme smallholder involvement in the programme | |

| Compliance support | 1. Program to support high-risk mills (mills located in areas at high risk of contributing to deforestation) to become compliant. |

| ZDCs should provide clear and functional assessment and engagement mechanisms. | |

| 2. Regularly engages with high-risk mills | |

| Monitoring mechanism | 1. Available and open grievance or complaint system |

| ZDCs should provide reliable and frequent monitoring systems. | 2. Self-reported evidence of monitoring deforestation |

| Transparency | 1. Disclosing the details of complaints and grievances, which includes the action and the status of enforcement. |

| ZDCs should allow for transparency in their enforcement approach. |

a Criteria in italic pertain to the progress of commitment implementation by companies, which is included in analyzing the quality of companies' ZDCs.

2.2. Defining spatial and functional fit

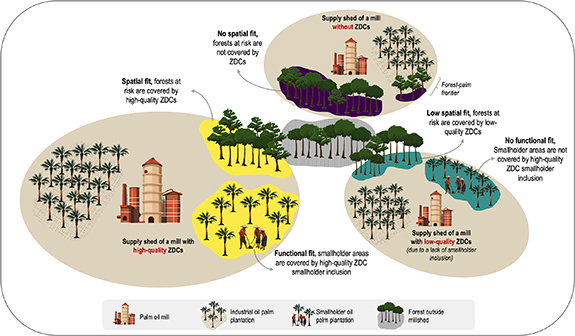

The concepts of spatial and functional fit form part of the more general framework of institutional fit [41], which examines mismatches between environmental governance, institutions, or policies, and the problems and socio-ecological contexts they intend to address [34, 41]. Institutional fit has primarily been studied regarding the state's role in managing ecosystems [34, 37]. However, the state's ability to manage resources is often limited due to scale mismatches and a lack of non-state actor involvement [42]. In consequence, scholars have advocated for expanding such frameworks beyond the state domain to address global-scale environmental challenges [35]. Expanding upon van Koppen and Bush [35] and Coenen et al [36]'s prior work in adapting spatial fit to the context of globalized commodity flows, we assess both spatial fit and functional fit in the context of palm oil supply chains to account for both ecological and equity concerns arising from ZDC policy design and implementation in distant producing areas.

Figure 2 depicts the conceptualization of spatial fit and functional fit. A spatial overlap between forests at risk and the supply shed of mills with high-quality ZDCs indicates spatial fit, whereas a lack of coverage of forests at risk by ZDCs indicates a lack of spatial fit, which may mean that ZDCs will have minimal effects on preventing palm-driven deforestation. We evaluate functional fit by evaluating whether mills that have smallholder plantation areas in their supply sheds have ZDCs that include a smallholder inclusion effort via providing support programs. Functional fit is shown in areas where smallholders are covered by ZDCs with high smallholder inclusion criteria, via which adverse livelihood impacts may be averted.

Figure 2. Conceptualization of spatial and functional fit of ZDCs. The colors used to delineate areas with or without spatial and functional fit in this conceptual framework are the same as the colors used in illustrations later in this paper. Yellow, turquoise, and purple represent high-quality, low-quality and no ZDCs, respectively.

Download figure:

Standard image High-resolution image3. Methods

3.1. Study area

The broad geographical scope of the spatial and functional fit analysis includes the three largest palm oil-producing islands in Indonesia: Sumatra, Kalimantan, and Papua. In 2019, Sumatra had the least forest cover (12 Mha) and the most oil palm plantations (9.5 Mha). Papua, on the other hand, had few oil palm plantations (nearly 0.3 Mha) and hosted substantial forests (34.3 Mha). Kalimantan stood in between with 25.7 Mha of forest cover and 6 Mha of oil palm plantations [1].

3.2. ZDC quality and links to mill supply sheds

We evaluated ZDC policy quality using indicators drawn from SPOTT (the Sustainable Palm Oil Transparency Toolkit), a non-profit platform that monitors company pledges and implementation [40]. To link company ZDC scores to the mills they own or source from, we utilized TRASE [43], a tool that maps company supply chains and ownership patterns by combining information from trader and refiner self-disclosure traceability reports with a database of known Indonesian palm oil mills [44].

3.2.1. Assessing ZDC score

We evaluated the quality of ZDC commitments of these 51 companies by assessing each company's performance on 15 relevant indicators from SPOTT, with 9 assessing policy completeness and 6 evaluating policy implementation (supplementary table 1S). We classified companies as having high-quality ZDCs, low-quality ZDCs, or no ZDCs ('zero'), using the following conditions:

- 1.If a company has not adopted a ZDC for all suppliers, it is classified as zero.

- 2.If a company has a ZDC for all suppliers and meets some, but not all, criteria thresholds, it is classified as low-quality.

- 3.If a company has a ZDC for all suppliers and meets all criteria thresholds, it is classified as high-quality.

We used a threshold approach rather than a simple additive index because we consider that the six categories of performance that we identified have to work together in order to achieve effective policy outcomes and cannot be traded off against each other. Still, given the variation in approaches, in certain categories we allowed for multiple avenues to meet a threshold (via either-or criteria). All included indicator thresholds are listed in table 1S. For numerical analyses such as interpolation and performing statistical tests, we converted the 'zero', 'low-quality', or 'high-quality' categories into numeric scores of 0, 1, or 2, which preserves the ordinal value. We also calculated the ZDC scores for 2018 and 2019, in addition to the 2020 score [45].

3.2.2. Determining mill-level exposure to ZDCs

In 2020, 1218 mills were in operation in Indonesia [43], with 1172 mills listed in Sumatra, Kalimantan, and Papua. After excluding mills with both unidentified owners and buyers, we were left with 1063 palm oil mills in Sumatra (n = 691), Kalimantan (n = 359), and Papua (n = 13), representing 87% of operational mills. The TRASE data indicates these mills are owned by 188 corporate groups, and sell to 28 corporate groups. Since some corporate groups can act as both owners and buyers, these links generated a list of 198 corporate groups operating in the Indonesian palm sector.

To link mills and their supply sheds to corresponding ZDCs, we differentiate between a ZDC 'owner' score that refers to internal company requirements via corporate ownership and the ZDC 'buyer' score that measures external supply chain pressure via purchasing links.

For the 'owner' score, we attributed companies' calculated ZDC scores directly to mills that they own. Our analysis focuses on the mills with known ownership (n = 912), of which 59% (n = 536) owned by 49 corporate groups were matched to the 51 companies we assessed.

We calculated each mill's 'buyer' score as the weighted mode of the ZDC scores of the refinery groups sourcing from the mill that we can identify in the TRASE data (i.e. known buyers). We assigned weights according to estimated sourcing volumes in 2020 [43] from known buyers, meaning that the score assigned at the mill level is the score with the cumulative highest volume in total, thereby representing the majority of the known buyers. This method acknowledges the market realities where companies handling larger volumes tend to have a stronger market presence and exert greater economic and policy influence on mills. Out of 988 mills linked to 28 corporate groups, we matched 22 corporate groups, which source from 985 mills, to the 51 assessed companies. Thus, each mill point may have a ZDC score by mill owner, by buyer(s) or both depending on data availability in the TRASE dataset.

3.2.3. Determining grid-cell exposure to ZDCs

To delineate the geographic scope of ZDCs, we estimated each mill's sourcing area or mill shed within grid cells of . Palm oil sourcing zones by island were determined using inverse distance weighting with a sourcing distance of 38 km, based on the 97.5th percentile of the distance between oil palm plantations and the nearest palm oil mill. Past work has used this radius approach [2, 25, 46, 47]. Our identified sourcing distance of 38 km aligns with previous estimates, e.g. [2] used 30 km for Sumatra, and Starling 6 uses 2, 20, and 50 km [47]. We used an inverse distance weighting method to assign ZDC scores to all grid cells within each mill shed based on each mill point's owner and buyer ZDC score and analyzed ZDC owner and buyer scores separately.

3.3. Operationalizing spatial and functional fit

To estimate spatial fit, we combined our estimates of grid-cell level ZDC scores with an analysis of the extent of remaining forests and their conversion risk. We furthermore overlaid the grid-cell level ZDC smallholder inclusion score with the extent of independent smallholder production areas to measure functional fit.

3.3.1. Remaining forest cover

We define remaining forests as areas in a 30 m resolution pixel with over 30% tree cover in 2000 from the data by Hansen et al [48] that were not identified as timber, rubber, mixed crop plantations [49] or oil palm plantations [1] and that were not lost by 2020. We chose this threshold to be inclusive of highly disturbed, recovering, and regrowing forests which could be deemed potential high carbon stock forests (supplementary table 2S). Previous studies applied tree cover thresholds from 30%–90% [1, 25, 48, 50].

3.3.2. Deforestation risk from industrial oil palm expansion

We developed maps of industrial oil palm plantation expansion [51] probability circa 2020 using a Bayesian Weights of Evidence (WOE) approach [52] in the environmental modeling software Dinamica EGO [53]. These maps should be understood as representing the relative likelihood of expansion within each island region, showing how one pixel compares to other pixels in terms of the likelihood of expansion. We selected WOE above other possible approaches to develop probabilities because it need not conform to assumptions of parametric methods [54], it is readily available for use in Dinamica EGO which is capable of handling the multiple large maps used in this project, and the method has been successfully applied to predict land cover change including oil palm expansion in Indonesia [54, 55]. We first selected several spatially heterogeneous factors that are thought to influence industrial oil palm expansion [1], including continuous and categorical variables (described in supplementary text and summarized in supplementary table 3S), and resampled them to identical 100 m spatial resolution grids before analysis. Since the WOE approach requires that all variables are categorical, we then classified continuous variables following Rivero's approach [56].

Then, we calculated the WOE score (see table 4S) for each category for all variables for all industrial oil palm expansion events from [1] from 2011–2012–2019–2020. By using multiple years to compute WOE, we avoided overfitting the model to any single year. WOE were computed separately for Sumatra, Kalimantan, and Papua regions. Next, we combined the WOE from each of these three geographic regions to create circa 2020 industrial oil palm expansion probability maps by applying the following calculation to each map location:

Here, P is the probability of oil palm expansion in 2020 given weights (w) 1 through . We removed satellite-derived year 2020 smallholder oil palm [1] and non-forest areas (previous section) from these probability maps such that expansion probability was only computed in non-oil palm forested areas. We then calculated the average probability of forest conversion to oil palm within each mill supply shed.

3.3.3. Smallholder production

We map the extent of independent smallholder plantations in 2019 using the most recent palm oil map [57] and extracting areas classified as 'smallholder' in the dataset. Plasma plantations were categorized as 'industrial' plantations in the dataset, due to pattern similarities, so they were not included in this layer. We selected smallholder plantation areas that were within the estimated mill shed areas.

4. Results

4.1. ZDC adoption is widespread, but many companies fall short on traceability, smallholder inclusion, compliance support, and transparency

As of 2020, over 70% of assessed companies (36 out of 51) had adopted a ZDC. Of these, 14 companies had high-quality ZDCs while 22 had low-quality ZDCs, with an average of 4–5 categories in which they met the minimum threshold. Half of the companies with low-quality ZDCs had insufficient scores on traceability, compliance support, and transparency, while 55% failed to meet smallholder inclusion criteria. As seen in figure 3, mill owners predominantly fell short on traceability and transparency, whereas buyers most frequently failed to provide compliance support to high-risk mills. Interestingly, for both groups, smallholder inclusion in ZDCs was a weak spot. These four categories are crucial for tracing and supporting suppliers, including scheme smallholders, independent smallholders, and mills that pose a high risk for potential deforestation, so that they can comply with companies' sourcing policies.

Figure 3. Company groups by ZDC quality. (a) All company groups by ZDC quality in 2020, differentiating between owners and buyers. (b) Number of companies with low-quality ZDC (n = 22) by category, differentiated by above and below the quality threshold for each category, also differentiated by owners and buyers. Assessed companies were matched to mills as mill owners and/or buyers. For visualization purposes, those matched as mill owners were categorized as owners (left) and those matched as buyers or both mill owners and buyers were categorized as buyers (right). However, in the analysis, companies holding dual roles, both as mill owners and buyers, were included in both analyses for ZDCs by mill owners and buyers. In graph (a), high-quality, low-quality, and zero ZDC are marked in yellow, turquoise, and purple, respectively. Out of 36 companies with ZDCs, 19 were classified as owners, and 17 were classified as buyers. For each category, owners (left graph, n = 12) and buyers (right graph, n = 10) that meet the threshold are marked in yellow and those below the threshold are marked in turquoise. In graph (b), some components of ZDCs were not applicable for a few companies (e.g. some mill owners do not source from mills and thus do not perform risk assessment for mills and a few companies did not source from smallholders making smallholder inclusion components not applicable).

Download figure:

Standard image High-resolution imageAs our ZDC score includes criteria for both policy design and implementation, we can also compare companies' respective scores for these four low-performance categories. We find that for companies with low-quality ZDCs, the average policy design scores are generally higher than their implementation scores. Companies with high-quality ZDCs have a similar pattern, except on traceability (see figure 1S).

4.2. Buyers send more widespread signals than mill owners in Sumatra and Kalimantan, but have a weaker influence in Papua

In Sumatra, Kalimantan, and Papua, mill owners and buyers with ZDCs show a stronger presence at the grid level than non-ZDC companies. Mill owners with ZDCs cover 59% of all supply sheds (36% 'low' and 23% 'high') while buyers provide more widespread coverage at 83% (16% 'low' and 67% 'high'). This leaves 41% and 17% of supply sheds under 'zero' coverage due to owners and buyers without ZDCs, respectively, which indicate that buyers generally send stronger signals than mill owners (see figure 4). However, ZDCs vary spatially; while buyer ZDCs have better coverage in Sumatra and Kalimantan, they are less prevalent in Papua, where mills sell predominantly to buyers without ZDCs.

Figure 4. ZDC coverage within palm oil mills' supply base by (a) mill owners and (b) buyers; (c) ZDC coverage of supply sheds by mill owners and buyers in Sumatra (left), Kalimantan (Indonesian Borneo, center-left), and Papua (right). The three levels of coverage—high-quality, low-quality, and zero ZDCs—are presented in yellow, turquoise and purple, respectively. Areas outside of matched mill supply sheds and Sulawesi are indicated in white. Our analysis does not include the island of Sulawesi (center-right), which is highlighted in white.

Download figure:

Standard image High-resolution image4.3. 77% of forests at risk of conversion are not covered by high-quality ZDC policies of mill owners

So far, we have considered buyer and owner ZDCs as independent. However, in reality, they are strongly interlinked—in practice, one of the main ways in which buyers attempt to implement and enforce their ZDCs is to encourage or pressure mill and plantation owners to adopt their own commitments and align supplier policies [17]. This is because mill owners have direct influence on expansion decisions within the concessions they lease. In addition, mill owners often have a direct relationship with smallholders [58], which allows them to enforce rules and/or provide capacity-building support. Hence, buyer ZDCs alone that are not matched by owner ZDCs are likely to have limited effect. In spite of this, there is currently much less data and analysis of owner ZDCs across the ZDC literature in Indonesia. For all these reasons, in the following analysis of spatial and functional fit we focus on the results of the owner ZDC scores in the main text, while also providing a high-level comparative overview of the results on buyer ZDCs. More extensive results on the spatial and functional fit of buyer ZDCs can be found in the supplementary information (section 4.3).

In line with the ZDC coverage results, when assessing the spatial fit, we find that buyers' ZDCs provide more extensive coverage for forests at risk (i.e. forests with at least some risk of conversion) compared to the commitments of owners. Within supply sheds, 62% of the remaining forest is covered by high-quality ZDCs from buyers, 18% by low-quality ZDCs, with the remaining 21% lacking ZDC coverage (see figure 3S). In contrast, the ZDCs of mill owners only protect 57% of the nearly 33 Mha remaining forest within the mill supply base; and much of this coverage comes from low-quality ZDCs.

We identified high spatial fit (i.e. coverage by high-quality ZDCs) for 7.7 Mha of remaining forest in Sumatra, Kalimantan, and Papua, collectively accounting for 23% of the total remaining forests within the mill sheds (figure 5(b)). However, in Kalimantan and Papua, those forests face lower conversion risk than those covered by low-quality ZDCs. The average conversion probabilities for low-quality ZDCs in Kalimantan and Papua are 0.59 and 0.46, respectively, indicating that forests most at risk of conversion are insufficiently protected by corporate policies. Although only 18% of the remaining forests within mill sheds in Sumatra are exposed to high-quality ZDCs, those forests have higher average conversion probability (0.49) than those exposed to low-quality and zero ZDCs. Furthermore, Kalimantan hosts a considerably larger remaining forest cover in existing mill sheds compared to the other islands; while also facing the highest risk of conversion, with an average probability of 0.54, higher than that of Sumatra (0.35).

Figure 5. (a) The spatial fit map (bottom panel) is the result of the spatial overlay between ZDC quality by mill owner score that are attributed to mill sheds (see figure 4) and forest at risk within the mill sheds (top panel). (b) Descriptive statistics of remaining forests and probability of conversion in 2020 in supply sheds with high-quality, low-quality, and zero ZDCs in Sumatra (10.4 Mha, left), Kalimantan (18.3 Mha, center-left), and Papua (4.3 Mha, right). The left x-axis shows the total remaining forest cover within the mill supply shed, while the right x-axis shows the average probability of conversion into oil palm in forest with high- quality (yellow), low-quality (turquoise), and no ZDCs (purple) for each island.

Download figure:

Standard image High-resolution image4.4. Smallholder inclusion gap in ZDCs by mill owners

We observed that 89% of independent smallholder plantations are covered by buyer ZDCs that address independent smallholder inclusion. However, when considering ZDCs by mill owners, this figure drops to only 46% (figure 6(b)). Most smallholder plantations in Indonesia are located in Sumatra (figure 6(a)); however, 34% of these areas are located within mill owners' domains that do not explicitly include independent smallholders as a consideration in their ZDC, and an additional 20% are located in mill sheds that completely lack ZDCs. Although Kalimantan is primarily dominated by industrial producers, with only 16% of plantations owned by independent smallholders [1], we noted a lower proportion (36%) of mill owners with a high smallholder inclusion score than in Sumatra. Interestingly, in the frontier region of Papua, over 50% of smallholder plantations are covered by ZDCs with high inclusion scores; however, we also see in figure 6(b) that there are as of yet very few smallholder areas in existence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 6. (a) The functional fit map (bottom) is the result of the spatial overlay between ZDC, particularly smallholder inclusion criteria, by mill ownership (top) and smallholder palm (middle). (b) Total area of smallholder oil palm in 2019 within supply sheds with high-quality, low-quality, and zero ZDCs (marked in yellow, turquoise, and purple, respectively) in Sumatra (left), Kalimantan (center-left), and Papua (right).

Download figure:

Standard image High-resolution image{kind=link}

5. Discussion

5.1. Addressing gaps in ZDC implementation

Our findings reveal that, while some companies have achieved success in creating and implementing comprehensive ZDCs, many fall short on traceability, smallholder inclusion, compliance support provided to high-risk mills, and transparency. It is intriguing that a significant number of companies continue to struggle with supply chain traceability, with only 41% of companies that have achieved full traceability to the mill level in 2020, despite the fact that traceability is considered a top priority by companies [15]. As one would expect, companies have greater visibility of supply chains they have higher control over. While a third of companies have full traceability from their own mills to associated plantations, only 6% of companies that source from third-party mills have achieved full traceability from supplier mills to plantation. This reinforces the findings of earlier studies [15, 17] that identified traceability to plantation as a common hurdle for companies. The lack of traceability may create an opportunity for 'laundering,' whereby deforestation-linked products can enter deforestation-free supply chains [59]. It also shows the distance between the current reality in Indonesia and the new requirements of the EU Deforestation Regulation, which requires firms to identify the land plots on which primary materials were produced, and provide associated geolocation information, before making products available, placing them on the market, or exporting them [60].

Another major challenge in designing comprehensive ZDCs is having a commitment that supports different types of smallholders, as well as a commitment to engage high-risk mills to improve compliance. Smallholders are heterogeneous, and providing differentiated programs for different types of smallholders may address the barriers or lack of capacity to comply [61]. These types of concerns have also been at the heart of many of the criticisms of the new EU Deforestation Regulation [18]. Yet, only 65% of firms have good policies and support for inclusion of independent smallholders. This challenge is consistent with previous research that highlights the difficulties companies encounter when synchronizing their commitments with their operations and when managing suppliers, particularly smallholders [16, 17, 62]. Improving smallholders' capacity to comply with stringent ZDCs may also prevent the risk of deforestation driven by more informal actors [16]. Similarly, a commitment to engage closely with high-risk mills can help them comply with ZDCs, yet three-quarter of companies lack a program specifically designed to engage with high-risk supplier mills.

5.2. ZDC policies should be geographically and functionally targeted to cover areas of concern

Between 56% and 87% of remaining forests are in mill sheds with ZDCs by mill owners and refineries. However, less than a quarter of remaining forests are in mill sheds where mill owners have adopted high-quality ZDCs; and these forests had a lower risk of conversion compared to forests under low-quality ZDCs. This means that despite a perception of high ZDC dissemination in the Indonesian palm oil sector, there are still many areas that are not well covered by these supply chain policies. Stringent ZDCs are needed, especially in areas where high forest cover is at high risk of conversion. These conditions are mainly observed in Kalimantan, which holds 75% of remaining intact forests located inside of mill sheds. ZDCs could have the greatest impact on preventing expansion in such areas, but currently, they remain lacking.

There is a significant gap between the adoption of comprehensive ZDCs by mill owners and the refineries that buy from these mills. This results in an imbalance in coverage, with at-risk forests being exposed to greater ZDC coverage through downstream buyers than directly through local mill owners. This is unsurprising given that pressure from civil society has been heavily directed towards large firms [63] and confirms calls within ZDC studies on soy and beef to expand ZDC adoption among small and medium-sized firms [31, 64]. While targeting refineries did succeed in getting broad exposure to ZDCs across Indonesia, such indirect exposure to ZDCs might have less of an impact on land use decisions unless it is matched by ZDC adoption by their suppliers. Expanding ZDCs to small- and medium-sized oil palm growing companies might yield greater impacts both on forest protection and smallholder inclusion outcomes. Many mill groups own a network of mills and plantations which have more long-lasting purchasing relationships (allowing for higher influence over land use decisions) and contribute directly to land use trajectories. In frontier areas where palm oil development is still in the early stages and deforestation can be prevented, these actors hold more influence than buyers. Most developments in Papua are industrial concessions [65]. Furthermore, such actors possess the necessary resources, knowledge, and capabilities to provide training or programs for smallholders and high-risk mills to reduce the risks of marginalization of smaller producers. Therefore, it is imperative for both mill companies and buyers to adopt and implement stringent ZDCs.

6. Conclusion

We highlight four weaknesses in corporate ZDC design and implementation: traceability, smallholder inclusion, support for high-risk mills to ensure compliance support and transparency. Policy design scores tend to outperform implementation criteria, while smallholder inclusion is a common hurdle for companies. Though mill owners' and buyers' ZDCs show a substantial presence and cover 59% and 83%, respectively, of the supply base, approximately 77% of forests at risk of conversion to oil palm are in the supply sheds of mills whose owners did not adopt strong ZDCs. Furthermore, 54% of smallholder areas within the supply base are covered by ZDCs that do not include policy support for smallholder capacity-building, which may put them at risk for supply chain exclusion. While our results provide valuable insights based on companies' commitment and reported progress, we acknowledge that the actual implementation on the ground may present additional nuances. Thus, it is important to recognize that our findings likely represent the upper limit of policy comprehensiveness as well as spatial and functional fit, and that on the ground the gaps in implementation and coverage might be even more dire than identified here.

Limitations to our approach which future research could examine in further detail include: (i) expanding the spatial scope to smaller islands and other countries; (ii) conducting more fine-grained analysis of influence of mills on supplier plantations; and (iii) conducting impact evaluations of ZDC effectiveness, equity and spillovers. While our current approach is helpful to estimate the current ZDC coverage, mills only have direct influence over what is within their concession or indirectly on supplier plantations, and do not control all lands in their mill sheds. Hence, deforestation-free commitments should extend beyond the sourcing areas to protect ecologically sensitive areas, e.g. via participation in jurisdictional approaches, in which companies and governments collaborate to make entire regions more sustainable [15, 66, 67].

Despite the limitations, our findings carry three key policy implications. First, there is an urgent need to address common weaknesses in ZDC policy design and implementation to ensure comprehensive ZDCs (i.e. traceability, compliance support, transparency, and smallholder inclusion). Second, it is imperative to align the ambition of ZDCs by mill owners with those of buyers to improve the spatial coverage of ZDCs. Expanding ZDC adoption to mill owners (who are closer to implementation areas where agricultural practices, smallholders and at-risk areas exist) enables efficient targeting of capacity-building efforts and improves forest protection. Third, ZDCs should be strengthened among companies working in landscapes with the most at-risk forests. Ensuring such policy diffusion to reach critical areas on the ground will be important to drive meaningful impacts. These conclusions are particularly relevant in the context of the move from voluntary to mandatory supply chain regulation via the EU Deforestation Regulation. Without complementary improvements in ZDCs, the EU Deforestation Regulation will face numerous compliance and additionality challenges and may lead to numerous negative unintended consequences, including both deforestation leakage and negative equity impacts on smallholders [18, 68].

Data availability statement

The data and code that support the findings of this study are openly available at the following URL/DOI: https://doi.org/10.5281/zenodo.10609765.

Funding and acknowledgments

A C, J G, and M S were supported by S N F Grant #100017_192373 awarded to R G. R G was supported by the European Union (ERC, FORESTPOLICY, #949932). K C was supported by US National Science Foundation Grant #1739253. R H and J B acknowledge their collaboration with the Trase Initiative, which was supported by Gordon and Betty Moore Foundation Grant #7703.01 and David and Lucille Packard Foundation Grant #2022-74104. We thank the anonymous reviewers and the editors for their helpful comments. Views and opinions expressed are however those of the author only and do not necessarily reflect those of the European Union or the European Research Council Executive Agency. Neither the European Union nor the granting authority can be held responsible for them.

Conflict of interest

The authors declare no conflict of interest.

Credit authorship contribution statement

A C: Conceptualization, Methodology, Data curation, Investigation, Formal analysis, Writing—original draft, Writing—review & editing, Visualization. R G: Conceptualization, Investigation, Methodology, Writing—original draft, Writing—review & editing, Funding acquisition. K C: Conceptualization, Investigation, Data curation, Methodology, Writing—original draft, Writing—review & editing. R H: conceptualization, Data curation, Investigation, Writing—review & editing. M S: Conceptualization, Investigation, Data Curation, Writing—review & editing. J B: Data curation, Investigation, Writing—review & editing. J G: Conceptualization, Investigation, Methodology, Writing—original draft, Writing—review & editing, Visualization, Funding acquisition.

Footnotes

- 6

Starling, developed by Airbus and Earthworm Foundation, is a monitoring platform that provides land use data for improving supply chain or forest projects transparency.